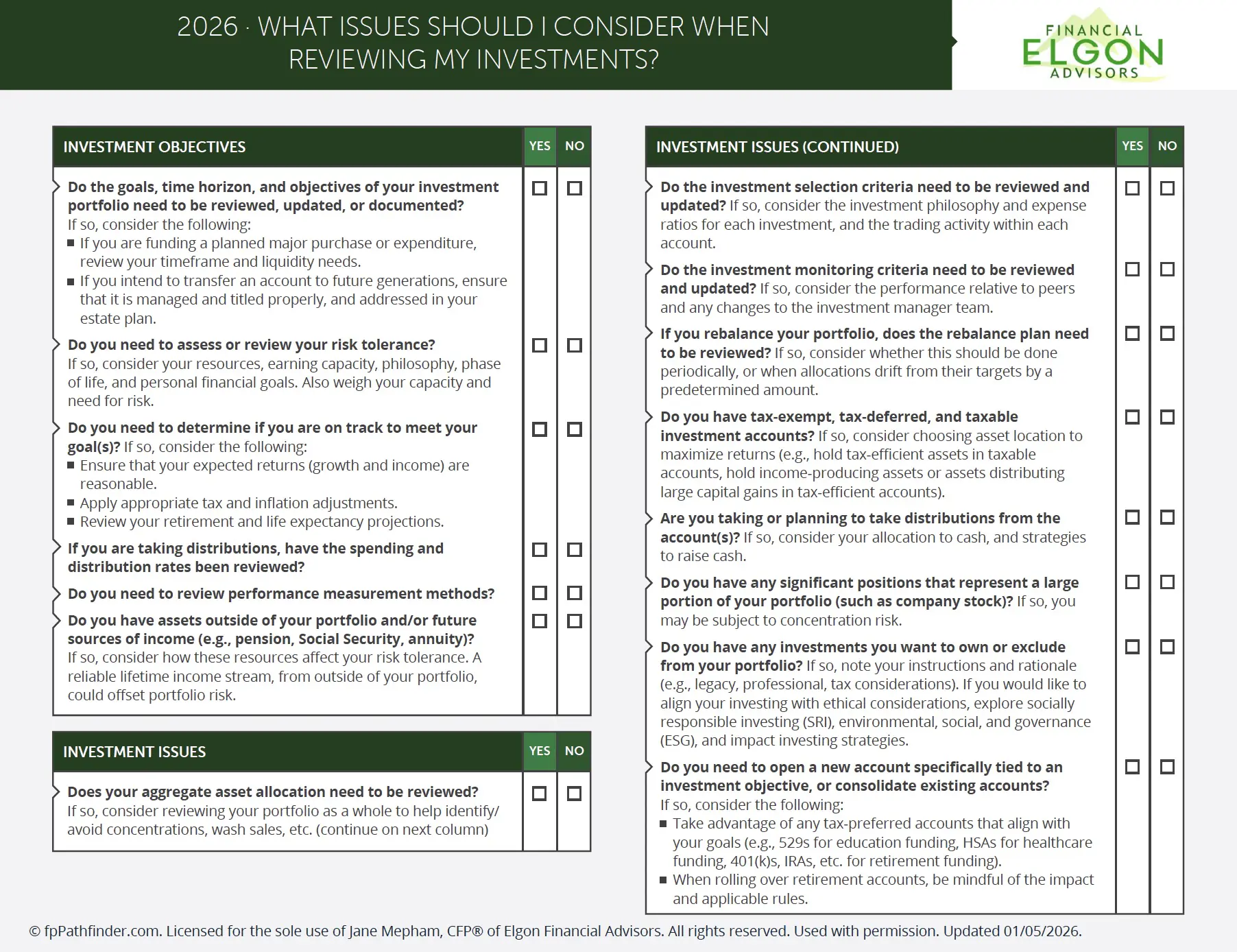

If you are a US resident, regardless of where you were born or where you reside and you have some type of foreign account, you might need to file an FBAR (Foreign Bank and Financial Accounts Reporting), as part of your tax filing process.

Photo by rupixen.com on Unsplash

In this post, I’ll discuss the top 5 things you need to know about this form/report. I’ll go into the what, the who, the where and how, and the why and the consequences for not filing it if eligible.

What’s the FBAR?

The U.S is one of the few countries that taxes citizens and permanent residents on world-wide income. The country of residence does not matter, and so as Americans have become more mobile, a lot of folks are finding themselves in the situation where they own all kinds of assets overseas. For example, an American family living abroad has bank accounts in those countries.

By the way, IRS knows exactly what you own overseas, so best to make peace with that.

A lot of first-generation Americans or immigrants – those born outside the U.S. still have substantial assets in their countries of origin. Second-generation Americans have also found themselves inheriting assets overseas or getting added as joint owners and this needs to be reported.

The joint account issue is more prevalent, where because of age or cultural practices, the kids who are living in the U.S. get added as joint owners to parents/families’ accounts in their home countries.

They don’t control the accounts, they are not meant to do anything with the accounts and won’t have access to the funds in the accounts, until the parents pass away. Unfortunately, because this now show up as being owned by a U.S. person, they must be reported to the treasury department.

The overseas asset ownership issue is a key point to discuss with your CPA or Financial Planner when it comes to assets outside the U.S.

To report the accounts, you use an FBAR which stands for Foreign Bank and Financial Accounts Reporting. The report is filled out on Form FinCEN Form 114.

What it’s Not

I do want to make it clear that the filing is information only. There are no taxes or fees due when you file the form.

Who Should File the FBAR?

If you meet the following conditions, then you should file the FBAR.

You are a U.S. citizen, or a permanent resident or you fit the description of a tax resident and own, or control funds or are a nominee of a financial account in a country overseas and the account balance at any one point in the year is more than $10,000.

Examples of the accounts are bank accounts, securities accounts like retirement accounts, any type of investment account, brokerage accounts, and life insurance (cash value) accounts.

If you have multiple accounts and each is less than $10,000, but the combined balance is over the $10,000 threshold then you need to file the FBAR.

For example, Sunil is an NRI (Non-Resident Indian), who currently works and lives in the U.S. He maintains a fixed deposit account at the Bank of Baroda due to their attractive interest rates, as well as a way to channel money to other investments home. In addition, he also has a checking account at the same bank.

He maintains a combined balance under $10,000, but last month, the balance got to $10,100 for a couple of days before he moved the money. He’ll need to do an FBAR filing for these accounts when he files his 2021 taxes in 2022.

If the foreign account is in foreign currency, you’ll need to convert the amount into USD using the Treasury Reporting Rates of Exchange of the last day of the calendar year in question.

There are a few other forms that may be required depending on your balances I will address those in a separate blog.

Where and How to File the FBAR

The main connection with IRS is that the form is due April 15th following the calendar year reported. The information in the form may be required for tax filing, which is probably why the two have the same deadline. There is an automatic extension until October 15th, so if you miss the April date, you still have time to file.

The FBAR form is filed separately from taxes and is filed electronically. The website to file the form is The Financial Crimes Enforcement Network.

There are a lot of CPAs who now offer this as a separate service – check with your CPA if not sure how to go about filing.

In addition, if you haven’t filed the last couple of years and you should have been filing, it’s not too late, you can still file, but probably best to reach out to a CPA who does this work or a financial planner that understands this and can connect you with a CPA.

The Penalty For Not Filing the FBAR

Over the last couple of years, the treasury department has stepped up efforts to find assets in foreign banks. The 2010 Foreign Account Tax Compliance Act (FATCA), which was part of the HIRE Act, requires Foreign financial institutions like banks to report to the U.S. government on the foreign assets held by U.S. account holders or be subject to penalties and withholding.

Due to the fear of the penalties and withholding – which can be up to 30% on their US income, foreign banks have become more careful in determining U.S. Citizenship for their existing clients, as well as new clients.

The Bank Secrecy Act requires financial institutions to report cash transactions that exceed $10,000 on a daily aggregate amount. A lot of these regulations have been put in place to prevent and or stop money laundering. But it means the treasury department is aware of assets in foreign banks.

Failure to file the FBAR can lead to some very high fines. The IRS has a process to determine if the lack of filing was willful (on purpose) or non-willful to determine the penalty which could be up to 50% of the account’s value.

Last month the Journal of Accountancy profiled a case in which the courts upheld penalties close to a million dollars for a couple that failed to file FBARs for a couple of years and claimed to not know it was required.

This brings to mind the famous quote “Ignorance is no defense.”

You really don’t want to have to start explaining to the IRS, what you knew or didn’t know about your assets, please take care of your FBARs.

References

- https://www.irs.gov/newsroom/report-of-foreign-bank-and-financial-accounts-fbar-1. Accessed March 16th 2021

- https://www.fincen.gov/resources/statutes-regulations/fincens-mandate-congress. Accessed March 16th 2021

- https://www.irs.gov/businesses/corporations/information-for-foreign-financial-institutions. Accessed March 16th 2021

To continue being a part of the conversation on financial issues that affect immigrants subscribe to Elgon’s blog posts by email here.

PFICs Explained: Everything You Need To Know

PFICs are a big issue for foreign-born families with assets outside the country. They are taxed punitively, and the tax reporting is a compliance nightmare.

In today’s post, I’ll discuss PFICs (passive foreign investment company), their origin briefly, the taxation, and how tell if there is a PFIC lurking in your overseas accounts or not. Finally how to think about them if they are a part of your overseas portfolio.

The Intersection Of Immigration and Personal Finances – Visa Status

For foreign nationals on work visas or immigrants (green card holders or naturalized citizens, any financial decision needs to be looked through your immigration status.

In this post, we identify the three immigration status.

It’s Not Too Late To Lower Your 2025 Taxes Using These 6 Moves

It’s not too late to lower your 2025 taxes, or future lifetime taxes. There are specific things you can do now, I discuss six moves you can use right now.